RSS Feed

RSS Feed Twitter

Twitter

Aims to bring more transparency; May pave way for NBFCs, fintechs to enter the business

from The HinduBusinessLine - Money & Banking https://ift.tt/TvCgFBR

Read more »

from The HinduBusinessLine - Money & Banking https://ift.tt/TvCgFBR

12:09 PM

12:09 PM

Blogger

Blogger

7:11 AM

Blogger

The finance ministry has asked state-run banks to further bolster their balance sheets from markets, which will enable them to reduce reliance on the government to shore up their capital adequacy.

At a meeting with top executives of public sector banks (PSBs) on Friday, financial services secretary Sanjay Malhotra expressed optimism that the lenders, having registered good profitability in the first three quarters of FY22, will continue to perform well on relevant metrics in the coming years.

“The underlying idea behind the exhortation is simple. Strong banks, with adequate capital, will be able to lend more and help economic growth. The government’s focus is on credit flow,” a top banker, who attended the meeting, told FE.

The government was forced to infuse over Rs 3.3 trillion between FY16 and FY21 into state-run banks to help them cope with the bad loan crisis. For the current fiscal, however, the government hasn’t budgetted any capital infusion, after no state-run bank recorded loss in the first three quarters of FY22.

Malhotra also impressed on the PSBs to explore more tie-ups among themselves and asked large banks to share their best practices with small lenders and guide them where they need more support and expertise.

The meeting was part of the Manthan 2022 that was held after a gap of three years during which the pandemic battered several sectors of the economy, raising concerns about the asset quality deterioration of lenders once all the relaxations and forbearances granted by the central bank come to an end.

While credit flow has improved in recent months amid prodding by the government, bankers are yet to shun risk aversion considerably.

Non-food bank credit grew 8% in February, compared with 6.6% a year before. However, loans to industry grew at a slower pace of 6.5% even on a favourable base (it had risen just 1% in February 2021).

Improved financials enabled PSBs to raise a record Rs 58,697 crore from the markets FY21, which included an equity capital of Rs 10,543 crore. This was way above `29,573 crore raised by them in FY20. In the first eight months of FY22, PSBs raised as much as Rs 32,567 crore.

Importantly, PSBs recorded a net profit of Rs 48,874 crore in the first three quarters of FY22. This is higher than the profit of Rs 31,820 crore in the entire FY21, which was the highest in five years.

According to the RBI data on domestic operations, state-run banks’ gross bad loans dropped to 8.18% of gross advances by December 2021 from 9.36% as of March 2021. Their capital adequacy was about 14.3% as of June 2021, above the requirement of 10.875%. The financial services secretary also asked the chiefs of PSBs to firm up strategies to ensure long-term profitability and adopt even more customer-centric approach.

The Manthan 2022 was held to brainstorm with the top leadership of PSBs and unlock next-generation reforms while continuing with the so-called EASE (enhanced access and service excellence) initiative, according to a senior official with the Indian Banks’ Association. The first PSB Manthan exercise was held in 2014. The IBA is now spearheading the EASE initiative.

7:10 AM

Blogger

Indicating that there can be no clear road map of policy action, RBI governor Shaktikanta Das has said that the central bank’s monetary policy committee (MPC) needs to constantly re-assess the situation and tailor response accordingly as the situation is dynamic.

1:09 PM

Blogger

Indicating that there can be no clear road map of policy action, RBI governor Shaktikanta Das has said that the central bank’s monetary policy committee (MPC) needs to constantly re-assess the situation and tailor response accordingly as the situation is dynamic.

1:09 PM

Blogger

1:09 PM

Blogger

12:09 PM

Blogger

11:09 AM

Blogger

10:09 AM

Blogger

7:02 AM

Blogger

This was the first meeting between the two central banks after Russia invaded Ukraine on February 24. The officials assessed the technical hurdles faced by exporters and importers in the two countries.

6:11 AM

Blogger

This was the first meeting between the two central banks after Russia invaded Ukraine on February 24. The officials assessed the technical hurdles faced by exporters and importers in the two countries.

6:11 AM

Blogger

The share of failed auto-debit requests on the National Automated Clearing House (NACH) platform rose marginally to 29.6% in volume terms in March 2022, up 40 basis points (bps) from the previous month. In value terms, the bounce rate stood at 22.8%, up 36 bps from February 2022.

Bounce rates had been easing since November 2021 and had reverted to pre-pandemic levels earlier this year, as the economy opened up and borrowers’ ability to repay loans improved. The trend may have been reversed to an extent in March as rising prices of food and fuel hurt borrower finances, said two analysts tracking the financial sector. Also, delinquencies from some retail accounts restructured under the Reserve Bank of India’s (RBI) Covid-resolution schemes may have increased in March.

As per data released by the National Payments Corporation of India (NPCI), of the 97.93 million debit requests made in March over the NACH platform, 28.99 million bounced. Of the requests for Rs 97,801 crore, declines were to the tune of Rs 22,302 crore.

To be sure, some of the debit requests made by the NACH platform are not for EMI payments; the platform is also used for insurance premium deductions and systematic investment plan (SIP) mandates. Among the EMI mandates, requests from non-banking financial companies (NBFCs) and fintechs account for a chunky share.

“The rise in the bounce rate is minimal and it could be due to inflationary pressure on borrower cash flows,” said an analyst. The first set of fuel price hikes in four months began on March 22 amid heightened volatility in global crude prices.

Moratoria on some small-value loans restructured to address Covid-related stress expired in the January-March 2022 quarter, and part of the rise in delinquencies may have emerged from such accounts. Bankers say anywhere between 4-5% of such accounts have slipped into the non-performing asset bucket. Sector experts say the last few quarters’ improvement in bounce rates may not have fully reflected the level of stress within the financial sector. In a report on April 5, analysts at rating agency Icra said that challenges could emanate from the performance of the restructured loan book which poses uncertainty to asset quality.

Anil Gupta, vice-president, Icra, said, “Russia-Ukraine conflict poses macro-economic challenges related to cost inflation, higher interest rates and exchange rate volatility, this could pressurise asset quality. Elevated levels of overdue loans in retail and MSME segments post-Covid also remain a concern.”

10:10 AM

Blogger

9:10 AM

Blogger

9:10 AM

Blogger

Global growth momentum is dampened by prolonged inflation, supply chain disruption, volatility in energy markets and investor uncertainty, finance minister Nirmala Sitharaman has said as she attended the G20 finance ministers and Central Bank Governors (FMCBG) meeting here.

3:02 AM

Blogger

Global growth momentum is dampened by prolonged inflation, supply chain disruption, volatility in energy markets and investor uncertainty, finance minister Nirmala Sitharaman has said as she attended the G20 finance ministers and Central Bank Governors (FMCBG) meeting here.

3:02 AM

Blogger

It acquired a principal loan portfolio of ₹141 crore from Indian Overseas Bank at a reserve price of ₹84.8 crore under a structured deal of 25:75. Here, the ARC paid 25% of the transaction value upfront and the balance will be paid in the form of security receipts that will be redeemed as it recovers money from borrowers.

2:11 AM

Blogger

It acquired a principal loan portfolio of ₹141 crore from Indian Overseas Bank at a reserve price of ₹84.8 crore under a structured deal of 25:75. Here, the ARC paid 25% of the transaction value upfront and the balance will be paid in the form of security receipts that will be redeemed as it recovers money from borrowers.

2:11 AM

Blogger

The assets size of the country’s top banks has improved in 2021 with State Bank of India (SBI) and HDFC Bank climbing up two notches in the latest S&P Global Market Intelligence’s ranking of the Asia-Pacific’s largest banks. What’s more, the third-largest lender – ICICI Bank — has found a place in the league table with the rank of 50. The three lenders together have an asset size of $1.2 trillion, which is 2.1% of the aggregate assets of the top banks in Asia.

The ranking, which was based on the total assets, features the largest state lender SBI in 22nd position, whereas HDFC Bank occupied the 44th slot in the latest ranking. Among the top 25 lenders, only SBI and Industrial Bank Co of China have seen two notches jump in the ranking.

“Banks in the Asia-Pacific face uncertainties from the Russia-Ukraine conflict and divergent monetary policies in the region. The rising pace of inflation, fueled by higher commodity prices, has pressured the region’s central banks to follow the US Federal Reserve and end ultra-loose monetary policies. Still, many central banks, especially in China, see the need to support their economies as they continue to face the drag from the Covid-19 pandemic,” observed S&P Global Market Intelligence.

However, nearly half of the list is dominated by Chinese lenders whereas Japan comes second with eight banks featuring in the list. Twenty-two mainland Chinese banks made it to the list, holding combined assets of $34.526 trillion at end of 2021, rising more than 10% from a year ago. The combined assets of all 50 banks together stand at $56.32 trillion. South Korea and Australia have six and four lenders, respectively, featured on the ranking.

With 20.05% compounded annual growth in net income and similar growth in deposits, the total assets of HDFC Bank surged by 18.9% over the last five years to $267.12 billion at the end of 2021. While the total assets of SBI grew by 9.5% over the last five years, ICICI Bank saw its assets grow by 11.4% during the same period.

Nevertheless, the Indian banks boast of a higher rank in market capitalisation as of March 2022, with HDFC Bank commanding 7th rank in Asia pacific region. While ICICI Bank is ranked 14th on the list, SBI is occupied 17th rank.

2:02 AM

Blogger

Baring, which holds the credit for one of the early syndicated acquisition financing for a private equity fund when it bought technology firm Hexaware in 2013, is in talks with a group of banks including Nomura, MUFG, Investec, Barclays, Deutsche Bank and JP Morgan, three people with knowledge of the development told ET.

12:02 AM

Blogger

Baring, which holds the credit for one of the early syndicated acquisition financing for a private equity fund when it bought technology firm Hexaware in 2013, is in talks with a group of banks including Nomura, MUFG, Investec, Barclays, Deutsche Bank and JP Morgan, three people with knowledge of the development told ET.

12:02 AM

Blogger

In its letter dated April 19, the RBI stated that Fino Bank can carry out referral services of term deposit products in the form of FD and RD as a Business Correspondent of Suryoday Small Finance Bank (SSFB).

5:11 AM

Blogger

In its letter dated April 19, the RBI stated that Fino Bank can carry out referral services of term deposit products in the form of FD and RD as a Business Correspondent of Suryoday Small Finance Bank (SSFB).

5:11 AM

Blogger

One of the biggest challenges for small finance banks (SFBs) from a tech point of view is the lack of an automation process and the corresponding need for manual intervention. This makes the deployment of an integrated engagement platform vital to such entities. Such a solution breaks down organisational silos, allowing for a centralised view of customer profiles and sounder communication across channels. It also helps in easier collection of EMIs and installments from micro banking and retail loanees.

This is why Ujjivan Small Finance Bank went for digital onboarding of customers, tying up with MoEngage for the purpose. But the change wasn’t easy since most of its customers came from unserved and underserved segments, with some living in remote areas. So, the bank partnered with a few names in the telecom space whose outlets could be used by customers to repay their loans, with the same being reflected in their accounts in real-time.

Sriram Srinivasan, head of digital banking, Ujjivan Bank, explains: “Prior to implementing the customer engagement solution, most of our customer communications were done manually. After MoEngage’s implementation, the bank was able to save on additional manpower which was routed to business operations, optimising response time and driving revenue growth.”

Apart from improving operational efficiency and resource utilisation, the marketing teams at the bank were able to reduce their dependency on database teams as the customer and campaign data was readily available on MoEngage. “The teams also found that using push notification as a communication channel was economical, thus contributing to an efficient ROI and adding to the bottom line,” he says.

Ujjivan Small Finance Bank onboarded approximately 2,00,000 unique customers for digital payments, with more than Rs 123 crore of EMIs collected in just five months and the conversion rate from digital channels growing from 2% to a whopping 18%. The martech stack and engagement solutions have also helped the bank stay ahead of competition.

Yash Reddy, chief business officer, MoEngage, says, “Owing to the seamless product and use case fitment on Ujjivan Small Finance Bank’s side, there were no major implementation issues. In fact, the concerns of the infosec team were dealt with immediately to avoid any hiccups in the integration processes. End-to-end support from the customer servicing teams is what enabled a seamless integration.”

3:11 AM

Blogger

The surge in commodity prices in the wake of the Russia-Ukraine war may have turned out to be a boon for banks in India as lenders are now witnessing higher demand for working capital. The increased cost of raw materials has led to companies utilising their working capital limits and even seeking top-ups, according to bankers FE spoke to.

The credit offtake improved during FY22, with the gradual return of normalcy after two waves of the pandemic and despite a relatively milder third wave. Non-food credit extended by banks grew 9.7% year-on-year (y-o-y) as on March 25, according to data released by the Reserve Bank of India. Growth in credit to industry recovered to 6.5% in February 2022 from 1% a year ago.

Rajneesh Karnatak, executive director, Union Bank of India, said working capital limits which had been lying idle are now getting utilised. “Corporates who have been utilising their limits have also been coming for additional working capital because the cost of production has gone up. The availing has increased by about 10%,” he said. This trend has emerged in the last one or two months as the Covid situation improved and the Russia-Ukraine situation led to price increases, Karnatak said, adding that higher costs have led to better demand across sectors such as steel, textiles, pharmaceuticals, chemicals and thermal power projects.

In February 2022, State Bank of India chairman Dinesh Khara said the unutilised portion in the bank’s working capital loans had fallen to about 43% from 52% in September 2021.

Crude oil prices surged to a 14-year high of $133 per barrel in the first week of March, and prices have been volatile since then, hovering around $110 per barrel. Base metal prices, measured by Bloomberg’s base metal spot index, increased by 25% between September 2021 and March 2022.

“Rising commodity prices are certainly playing a part in the improved credit growth that you’re seeing. Utilisation is getting better and there is also more demand for LCs (letters of credit) by manufacturers,” said a senior banker with a mid-sized private bank.

Credit to large industry shrugged off an extended period of contraction and sub-par growth to grow 0.5% in February 2022, led by engineering, chemicals, food processing, leather, rubber and plastic products. According to the RBI, infrastructure credit, which accounts for 38% of the total industrial credit, grew 11.9% in February 2022, driven by the road and power sectors and the government’s capex push.

In its monetary policy report for April 2022, the RBI said the firming up of global crude oil prices was the main factor that impacted prices of industrial inputs such as naphtha, aviation turbine fuel, bitumen, petroleum coke and furnace oil. “They also contributed to double-digit inflation in high-speed diesel, which in turn drove up farm input price inflation. Other contributory factors comprise fertiliser prices that edged up in sympathy with international prices, and prices of some non-food articles that remained in double digits – raw cotton and oilseeds,” the report said. The price of electricity – a key input in both industrial and farm inputs – also increased sharply during the second half of FY22 in line with the revival in demand.

2:11 AM

Blogger

Poonawalla Fincorp has entered the digital consumption loan space through a partnership with KrazyBee, to offer small ticket personal loans to individuals, the company said.

Poonawalla Fincorp focuses on consumer and small business finance as a part of its strategy. The tie-up between both the entities is a step towards building a strong pact with partners which have demonstrated distribution at scale, and risk management capabilities along with their technology prowess.

“We are a digital-first, technology-led lender, and this partnership with KrazyBee is a natural fit to our business strategy. The partnership brings together two lenders which are obsessed with customer satisfaction and want to offer the best of customer experience to all their customers by leveraging technology,” CA Abhay Bhutada, MD, Poonawalla Fincorp, was quoted saying in a release.

The partnership with KrazyBee provides complete end-to-end digital consumer loans across the country. The partnership has seen a lot of traction within a month of its launch and the company projects disbursement of more than `1,000 crore in the current financial year.

“Our technology strength empowers our partners to provide seamless disbursement services,” Madhusudan E, CEO, KrazyBee said.

KrazyBee Services is a non-deposit taking non-banking finance company. KrazyBee along with KreditBee which is its technology platform and India’s largest consumption-based personal loan platform commands more than 20% market share of NBFC – Fintech disbursement in India. KreditBee and KrazyBee are supported by strong equity investors such as Premji Invest, ICICI Bank and Mirae Asset and have also raised debt from multiple partners such as HSBC, Bank of Baroda & Kotak Mahindra.

1:11 AM

Blogger

The Reserve Bank has announced a slew of regulatory changes for non-banking lenders by amending the October 2021 circulars on scale-based regulations, which have brought in large NBFCs almost on par with bankers when it comes to addressing their credit risk concentration.

The regulator on Tuesday issued four separate circulars: Large exposures framework for NBFCs — upper layer; Disclosures in their financial statements; Scale-based regulation for capital requirements – upper layer; and Regulatory restrictions on their loans and advances. These are improvements on the October 22, 2021, circulars.

On the large exposure framework with the upper layer, the regulator said these prudential guidelines are aimed at addressing credit risk concentration in NBFCs and are set out to identify large exposures, refine the criteria for grouping of connected counterparties and put in place reporting norms for large exposures.

The regulator said the sum of all the exposure value of an NBFC to a single counterparty cannot exceed 20 per cent of its available eligible capital base at all times.

However, the board can allow an additional 5 per cent exposure beyond 20 per cent but at no time higher than 25 per cent of its eligible capital base, if the NBFC has a board-approved policy, setting out conditions under which over 20 per cent exposure may be considered; and if it informs the RBI in writing the exceptional reasons for which exposure beyond 20 per cent is being allowed in a specific case.

But the new norms allow an NBFC into infrastructure financing can exceed the exposure limit by 5 per cent of its tier I capital to a single counterparty – means 30 per cent of the tier I capital — if the additional exposure is on account of infrastructure loan and/or investment in which case it can go up to 35 per cent.

However, the new norms retain the definition of tier I capital as defined in the master direction issued in 2016 for systemically important NBFC and said profit accrued during the year will be reckoned as tier I capital after making necessary adjustments as per the guidelines applicable.

Regulated entities have to obtain an external auditor’s certificate on completion of the augmentation of capital and submit the same to the Reserve Bank before reckoning the additions to capital funds, it said, adding an eligible capital base means tier 1 capital.

Large exposure means the sum of all exposure values measured to a counterparty and/or a group of connected counterparties if it is equal to or above 10 per cent of the eligible capital base, it said.

What has changed in the new circular is that the scope of application is applicable both at the solo level and consolidated level and exposure shall comprise both on and off-balance sheet exposures.

On the disclosures in NBFCs’ financial statements, the new circular makes it mandatory for them to make disclosures in financial statements in accordance with the new prudential guidelines, applicable accounting standards, laws, and regulations.

The additional disclosure requirements are in accordance with the scale based regulatory framework and are an addition to the disclosure requirements specified under other laws, regulations, or accounting and financial reporting standards.

The new disclosure requirements shall be effective for annual financial statements for FY23.

On the regulatory restrictions on loans and advances of NBFCs based on the scale based regulation, which was first issued on October 22, 2021, it said the new guidelines will come into play from October 1, 2022.

Under the scale-based regulation for NBFCs’ capital requirements — upper layer, they have to maintain an equity tier 1 capital of at least 9 per cent of the risk-weighted assets, wherein the common equity tier 1 capital will comprise the paid-up equity share capital, share premium resulting from equity shares, capital reserves representing surplus arising out of asset sales, statutory reserves, revaluation of reserves arising out of change in the carrying amount of property consequent to its revaluation in accordance with the applicable accounting standards.

All these may be reckoned as CET1 capital at a discount of 55 per cent, instead of as tier 2 capital under extant regulations.

But this is subject only if the property is held for its own use by the NBFC and it can sell it readily at its own will sans any legal impediment; if revaluation reserves are presented/disclosed separately in the financial statements and the value is realistic and are in accordance with applicable accounting standards and are obtained from two independent valuers, among others.

It also allows an NBFC to reduce the accumulated losses from CET 1, while profits in the current financial year may be included on a quarterly basis if it has been audited or subject to limited review by the statutory auditors. Further, such profits shall be reduced by the average dividend paid in the last three years.

Also, it allows deducting the entire losses in the current year from CET 1 (Common Equity Tier).

The new regulatory adjustments/deductions shall be applied in the calculation of CET1 capital if it is deducted from the sum of items for goodwill and other intangible assets, goodwill and all other intangible assets should be deducted from the common equity tier 1 capital.

Investment in shares of other NBFCs and in shares, debentures, bonds, outstanding loans and advances, including hire purchase and lease finance made to and deposits with subsidiaries and companies in the same group exceeding, in aggregate, 10 per cent of the owned fund of the NBFC.

1:02 AM

Blogger

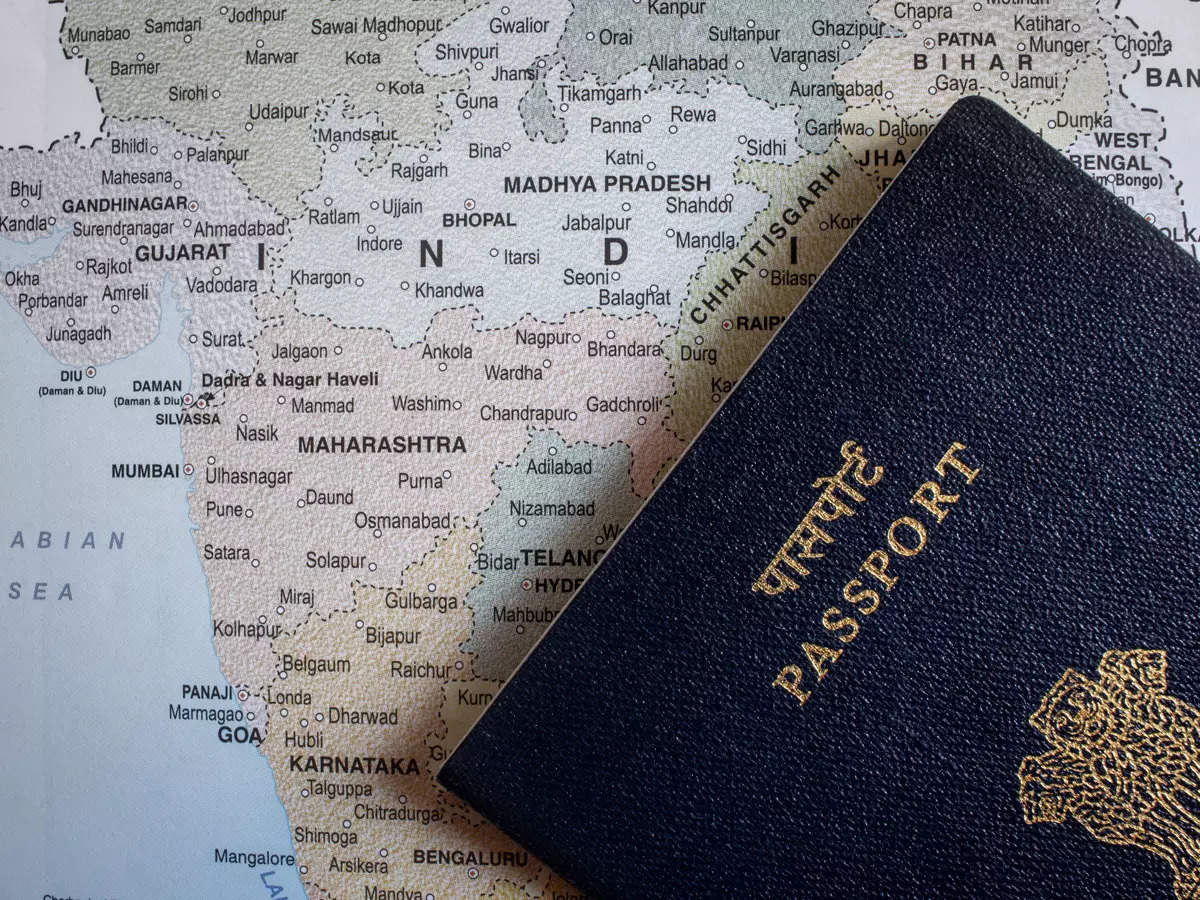

At present, passport details of promoters, directors and authorised signatories in respect of loan accounts of ₹50 crore and above must be furnished with the lenders.

12:11 AM

Blogger

At present, passport details of promoters, directors and authorised signatories in respect of loan accounts of ₹50 crore and above must be furnished with the lenders.

12:11 AM

Blogger

The Reserve Bank of India on Tuesday allowed Rural Cooperative Banks (RCBs) to raise funds from people in their area of operation or existing shareholders through a variety of instruments.

RCBs, which include state co-operative banks and district central co-operative banks, can raise funds from preference shares and debt instruments, RBI said in a notification.

RBI said the review is being done following the rural co-operative banks coming under the ambit of the amended Banking Regulation Act.

Such lenders can augment their capital through the issue of preference shares, which can include issue of perpetual non-cumulative preference shares which will be eligible for inclusion in core tier I capital. Besides, tier-II capital instruments, including perpetual cumulative preference shares, redeemable non-cumulative preference shares and redeemable cumulative preference shares can also be utilised.

According to RBI, they can also raise funds through debt instruments, including perpetual debt instruments eligible for inclusion in tier I capital and long term subordinated bonds eligible for inclusion in tier II capital.

Such RCBs need to adhere to certain conditions like not using their fixed deposit rate as a benchmark and make necessary disclosures prominently, especially ones saying the instruments under which the funds are raised are not fixed deposits.

The procedure for transfer to legal heirs in the event of death of the subscriber of the instrument should also be specified, RBI said.

7:02 AM

Blogger

Almost all lenders are now likely to follow the SBI in raising their benchmark rates, with the Reserve Bank of India (RBI) likely tightening monetary conditions to restrain inflation.

5:10 AM

Blogger

Almost all lenders are now likely to follow the SBI in raising their benchmark rates, with the Reserve Bank of India (RBI) likely tightening monetary conditions to restrain inflation.

5:10 AM

Blogger

4:02 AM

Blogger

4:02 AM

Blogger

At present, 50% of the bank's retail loans are sourced digitally. Out of this, 97% of the bank's personal loans are disbursed end-to-end digitally while the bulk of the home loan originations is done digitally.

2:02 PM

Blogger

At present, 50% of the bank's retail loans are sourced digitally. Out of this, 97% of the bank's personal loans are disbursed end-to-end digitally while the bulk of the home loan originations is done digitally.

2:02 PM

Blogger

This is the first offshore USD Secured Overnight Financing Rate (SOFR) linked syndicated loan raised by SBI through its Gift City branch, a release said.

1:09 PM

Blogger

This is the first offshore USD Secured Overnight Financing Rate (SOFR) linked syndicated loan raised by SBI through its Gift City branch, a release said.

1:09 PM

Blogger

12:09 PM

Blogger

8:11 AM

Blogger

The Reserve Bank of India’s (RBI) push to enable Unified Payments Interface (UPI)-backed cash withdrawals from ATMs is likely to cause a severe dent in the usage of debit cards, according to payment industry executives. Already a preferred mode of payments at storefronts and for small-value online transactions, UPI is now set to eat into the debit card’s last-remaining bastion of cash withdrawals.

At Rs 1.63 trillion, the value of merchant UPI transactions in February 2022 was well above the value of debit and credit card transactions at point of sale (POS) terminals, which was Rs 1.43 trillion. According to a recent report by HDFC Securities, UPI accounts for nearly three-fourth of all transaction volumes below Rs 500.

Harish Prasad, head of Banking, FIS, said that banks’ issuance of debit cards had seen significant growth over the last five to seven years, reaching 935 million outstanding cards as of February 2022. This may now start to flatten out as a consequence of high UPI use for merchant payments and saturation in card issuances.

“Also, with the recently announced interoperable card-less ATM cash withdrawal facility, using UPI based authorisation, as opposed to card and PIN based authorisation, and the announcement recently to allow activation of UPI via Aadhar OTP in lieu of a debit-card-linked OTP, the need for debit cards will be further diluted, and debit card numbers could likely start to shrink over the next few years,” Prasad said.

Cash withdrawals at ATMs are the chief means of usage for a majority of debit cards issued in India, with merchant payments using debit cards starting to plateau and even seeing volumes falling on a year-on-year basis. In February 2022, the number of debit card-based ATM transactions fell to 527 million from 551 million in February 2021.

Independent fintech expert Parijat Garg said that it may take banks a few months to upgrade their ATMs and other systems at the back end to offer UPI-based withdrawals. But once that happens, the utility of debit cards for a large number of customers will practically be gone.

“Only the online payments where people may not be too comfortable using UPI on a particular device or where it’s quite a large-value transaction or where the person is leveraging the benefits available on a particular debit card, such as debit EMI, might be the instances where a debit card is used,” Garg said.

Consumers may eventually see no point in carrying debit cards as there is an annual or quarterly fee for maintaining them but UPI is practically free. Garg pointed out that merchants also prefer UPI because it does not draw a merchant discount rate (MDR), but on debit cards at POS merchants have to pay around 1%. “The consumer demand for debit cards may eventually fall and banks may also find it costly to issue them in a scenario of low usage,” he added.

7:10 AM

Blogger

4:11 AM

Blogger

4:11 AM

Blogger

A pandemic-era shift to safer and better-rated assets resulted in a hit to margins and interest income in Q4FY22, HDFC Bank told investors. Supply chain issues in the vehicle segment and slower growth in credit card loans have resulted in a muted trend in retail loan growth, the bank’s management said.

HDFC Bank’s Q4 core net interest margin (NIM) of 4% counts among the lowest ever posted by the lender. Net interest income (NII) growth was also subdued at 10.2% year-on-year (y-o-y).

Srinivasan Vaidyanathan, chief financial officer of HDFC Bank, said on a post-results conference call that the bank’s asset mix has shifted towards higher-rated segments during the Covid period, albeit at lower yields. “As a result, NII growth has been lower but with the corresponding offset in credit costs which are lower than the historical average,” he said.

The ratio of NII to credit risk-weighted assets has improved over pre-Covid levels by approximately 20 basis points and is currently at around 7%, representing HDFC Bank’s optimised pricing for higher-rated segment volumes, Vaidyanathan added. The bank’s provisions fell over 29% y-o-y during Q4FY22.

HDFC Bank’s loan mix has shifted during the pandemic years in favour of wholesale assets, which now make up 55% of the loan book, as against 45% in 2019. The trend in retail was just the reverse, falling to 45% from 55% pre-Covid. Pricing in the wholesale market has become extremely fine of late as banks try to lure top-rated borrowers away from the markets.

Vaidyanathan said that HDFC Bank has traded off NIM for operating cost and credit cost to deliver sustained profitability. The lender chose to be risk-off all through the pandemic and it sees margin performance coming back over the next three to six quarters. “Retail is coming back, but wholesale has not relented. We need to get that opportunity which comes at a good quality. We are okay with that to the extent that it delivers the profitability that we require,” he said.

Growth in the retail segment is being hurt by the persistent shortage in supply of semiconductor chips, which are vital for vehicle manufacturing. In Q4 retail loans grew 5% sequentially for HDFC Bank as supply chain issues weighed on vehicle financing. Auto loans grew 9% y-o-y and 4% sequentially. Moreover, credit card customers showed a limited appetite for borrowing. While HDFC Bank’s card spending grew 28% y-o-y, credit card loans grew about 14% y-o-y and under 5% sequentially, below the bank’s historical average.

“We do believe that the vehicle (segment) should come back once the supply constraints abate. For the good part, it is coming back. The rate of growth we had this quarter on vehicles was better than the last quarter,” Vaidyanathan said. A similar trend is playing out in the credit card segment as well, he said, given that the Q4 numbers on spending and loan growth were an improvement over Q3FY22 when card spending grew 24% and credit card loans grew 9%.

2:11 PM

Blogger

Retail online transaction platform UPI will likely continue to dominate the digital payments space in the country even as newer methods such as BNPL and digital currency are expected to define the future of payments, a study has said. Unified Payments Interface (UPI), Buy Now Pay Later (BNPL), Central Bank Digital Currency (CBDC) and offline payments will drive growth of digital payments in India in the next five years, PwC India said in a report.

UPI is expected to continue to be the major contributor in the digital payments space, followed by BNPL, it said.

The Indian digital payments market saw steady growth at a CAGR of 23 per cent (volume wise), and is expected to reach 217 billion (21,700 crore) transactions in FY26 from 59 billion (5,900 crore) in FY22, said the report titled ‘The Indian Payments Handbook 2021-26’.

In 2020-21, UPI transactions reached a record 22 billion (2,200 crore), and it is expected to reach 169 billion (16,900 crore) by 2025-26, growing at a CAGR (compounded annual growth rate) of 122 per cent, it said.

Partnerships with other countries in Asia to enable low-value transactions and cross-border remittances through UPI will contribute to this growth. BNPL, which is currently estimated at Rs 363 billion (Rs 36,300 crore), is expected to reach Rs 3,191 billion (Rs 3,19,100 crore) by the end of 2025-26, according to the report.

“We expect the payments industry to focus heavily on enhancing customer experience and providing customer options for payment, enhancing security, undertaking innovations in technology like distributed ledger technology (DLT) and emerging tech like IoT (Internet of Things) over the next couple of years.

“With the efforts and initiatives of key stakeholders such as regulators, banks, payment/fintech companies, card networks and service providers, the industry is going to see tremendous growth in the coming years,” Mihir Gandhi, Partner & Payments Transformation Leader, PwC India, said.

Presenting a snapshot of the trends that will contribute to growth of digital payments industry in India, the report said that existing products and emerging use cases such as UPI, Fastag, transit (NCMC) and cards will continue to make inroads and gain additional wallet share of the Indian customers. These methods will continue to drive the growth in adoption and transactions numbers, said the report.

Enabling recurring payments and IPO subscriptions along with cross-border remittances will provide a boost to UPI. Parking and fuel payments are being explored as new use cases for Fastag, PwC report said further.

“The emergence of new players with a focus on digital journeys and expanding customer base in tier 3 and 4 locations will drive the growth for cards. Integration of NCMC with debit and credit cards alongside prepaid with news of public transport operators going live with acceptance infrastructure will bode well for the transit segment.”

Further, it said, with the RBI allowing to expand the scope of tokenisation to cover additional use cases like laptops, desktops, wearables, IoT devices along with card-on-file tokenisation (CoFT), with enhanced card-related security, will ensure that the overall customer check-out experience remains intact.

This is significant for leading merchants in grocery and retail, food delivery and apparel, among others who experience repeated purchase transactions from their customers, said the report. With regard to offline payments, PwC report said the recent RBI guidelines on offline payments have provided a much-needed impetus to the segment.

“Poor connectivity and lack of access to online payment methods have opened up an opportunity for offline payments. Efforts have been made by various players in the past to develop and deploy such solutions but with limited success.” They will give the necessary directions to the participants in developing offline payments solutions. Further, it will encourage banking and non-banking companies to collaborate with the solution developers, as per the report.

In the corporate payments space, financial institutions and service providers are offering payment solutions which can fulfil all the requirements of organisations and increase their operational efficiencies. Integrating payments into enterprise resource planning software that helps to automate essential business functions, and utilising payments data to improve operational efficiency and optimise essential processes are some of the use cases.

On the proposed CBDC, it said, given the present scenario, the central bank’s digital currency will need to co-exist along with the existing rails rather than replace them. “Some of the prominent use cases of CBDC that are applicable in the Indian context are programmable direct benefit transfer, online and offline retail payments and cross-border remittances,” it said.

2:02 PM

Blogger

Retail online transaction platform UPI will likely continue to dominate the digital payments space in the country even as newer methods such as BNPL and digital currency are expected to define the future of payments, a study has said. Unified Payments Interface (UPI), Buy Now Pay Later (BNPL), Central Bank Digital Currency (CBDC) and offline payments will drive growth of digital payments in India in the next five years, PwC India said in a report.

1:09 PM

Blogger

Retail online transaction platform UPI will likely continue to dominate the digital payments space in the country even as newer methods such as BNPL and digital currency are expected to define the future of payments, a study has said. Unified Payments Interface (UPI), Buy Now Pay Later (BNPL), Central Bank Digital Currency (CBDC) and offline payments will drive growth of digital payments in India in the next five years, PwC India said in a report.

1:09 PM

Blogger

10:02 AM

Blogger

The report further said, gradual increases in domestic interest rates will boost net interest margins because banks will be able to pass on higher rates to borrowers, while their funding costs will increase marginally because banks have reduced the share of high-cost corporate term deposits in total deposits.

7:11 AM

Blogger

The report further said, gradual increases in domestic interest rates will boost net interest margins because banks will be able to pass on higher rates to borrowers, while their funding costs will increase marginally because banks have reduced the share of high-cost corporate term deposits in total deposits.

7:11 AM

Blogger

HDFC Bank on Saturday reported a 22.8% year-on-year (y-o-y) growth in net profit for the quarter ended March to Rs 10,055 crore on the back of a 29% y-o-y fall in provisions to Rs 3,312.35 crore.

The country’s largest private bank saw its net interest income (NII) growing 10.2% to Rs 18,872.7 crore, while non-interest income grew just 0.6% y-o-y to Rs 7,637 crore due to losses and revaluation of assets in the investment book. A rise in bond yields during the fourth quarter was expected to hit banks’ treasury books.

The four components of other income for the quarter ended March 31 were fees and commissions of Rs 5,630.3 crore, foreign exchange and derivatives revenue of Rs 892.5 crore, loss on sale/revaluation of investments of Rs 40.3 crore and miscellaneous income, including recoveries and dividend, of Rs 1,154.7 crore.

The core net interest margin (NIM) in Q4 fell 10 basis points (bps) from the previous quarter to 4%.

This is among the lowest margin figures ever posted by HDFC Bank.

Total advances as on March 31 stood at Rs 13.69 trillion, up 21% over March 31 last year. Retail loans grew 15.2%, commercial and rural banking loans grew 30.4% and corporate and other wholesale loans grew 17.4%. Overseas advances constituted 3% of total advances.

Total deposits as on March 31 were Rs 15.59 trillion, an increase of 17% over March 31, 2021. Current account savings account (CASA) deposits grew 22% y-o-y, with SA deposits at `5.12 trillion and CA deposits at Rs 2.39 trillion. Time deposits stood at Rs 8.08 trillion, an increase of 12.3% over the previous year. The CASA ratio stood at 48.2%, up from 46.1% for the corresponding quarter a year ago.

The bank held floating provisions of Rs 1,451 crore and contingent provisions of Rs 9,685 crore as on March 31, 2022. Total provisions, including specific, floating, contingent and general provisions, were 182% of the gross non-performing loans as on March 31, 2022.

The gross non-performing asset (NPA) ratio fell nine basis points (bps) sequentially to 1.17% as on March 31, 2022, while the net NPA ratio fell five bps to 0.32%.

The bank’s total capital adequacy ratio (CAR) as per Basel III guidelines was at 18.9% as on March 31, 2022, (18.8% as on March 31, 2021) as against a regulatory requirement of 11.7%, which includes capital conservation buffer of 2.5%, and an additional requirement of 0.20% on account of the bank being identified as a domestic systemically important bank (D-SIB).

Tier 1 CAR was at 17.9% as of March 31, 2022, compared to 17.6% as of March 31, 2021. Common equity tier 1 capital ratio was at 16.7% as of March 31. Risk weighted assets were at Rs13.53 trillion, as againstRs11.31 trillion as on March 31, 2021.

The bank’s NBFC subsidiary HDB Financial Services posted a net profit of `427 crore in Q4FY22, down 17% y-o-y. Its total loan book grew 4% y-o-y to Rs 61,326 crore as on March 31, 2022. Stage 3 loans, denoting the ratio of bad assets, were at 4.99% of gross loans, down from 6.05% in the December quarter.

6:10 AM

Blogger

12:02 AM

Blogger

12:02 AM

Blogger

The funds will be raised in the period of next 12 months through private placement mode, subject to approval of shareholders among others.

The funds will be raised in the period of next 12 months through private placement mode, subject to approval of shareholders among others.